Logistic Regression

Conclusions up front

Reduced the model to 7 variables to predict credit fraud risk. Variables V4, V21, and V22 are roughly 2x increase to the likelihood of credit card fraud. Variables V10, V14, and V27 roughly reduce the likelihood of credit card fraud by half.

This is a logistic regression analysis on Credit Card Fraud Detection, using a dataset from Kaggle.com

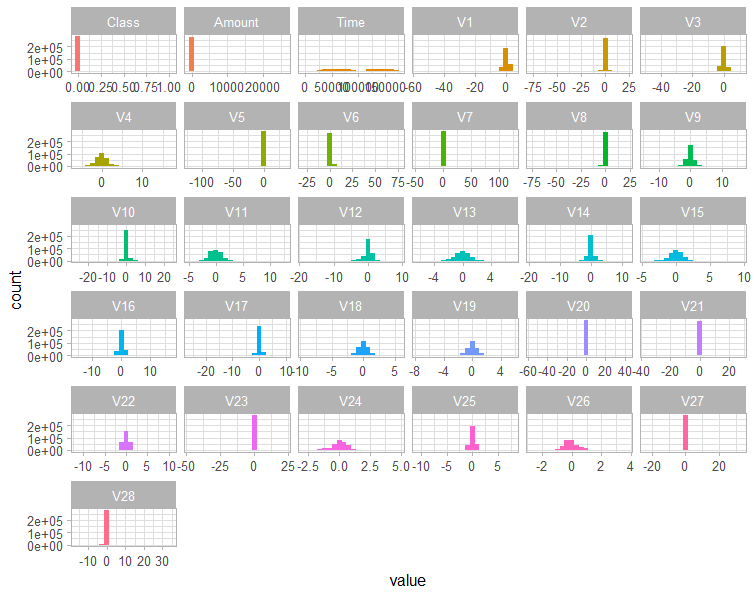

creditcard.csv > glimpse(CCFraud) Rows: 284,807 Columns: 31

Target = “Class”, a binomial target where 0=not fraud, 1 = fraud.

30 Variables include Time, V1 thru V28, and Amount. All variables are numeric, and variables starting with ‘V’ lack description due to data confidentiality.

Libraries loaded: tidyverse, GGally, ROCR, caret, funModeling, skimr

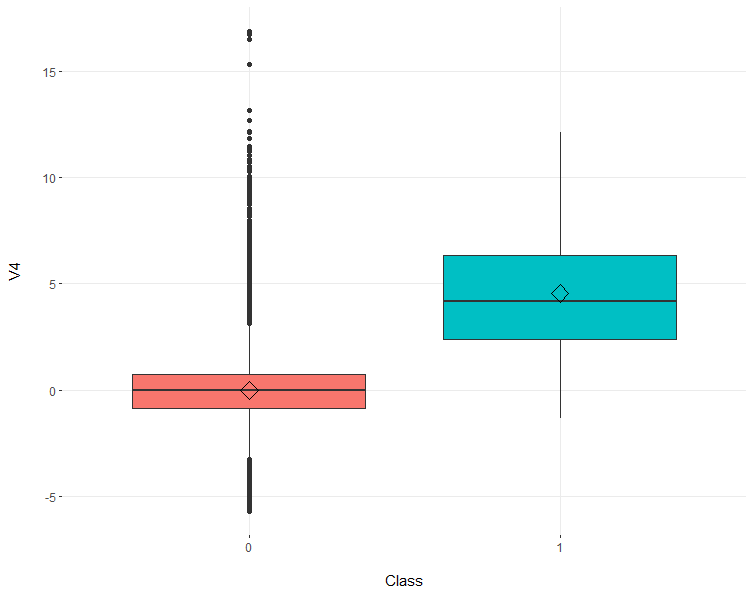

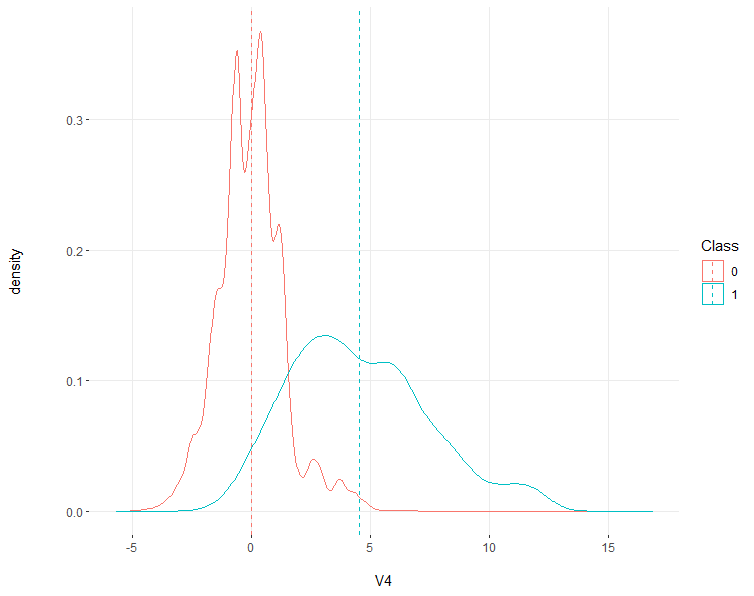

Credit Card Fraud (Class = 1) has an average V4 of ~4, whereas non fraudulent credit card charges (Class = 0) have an average V4 of 0.

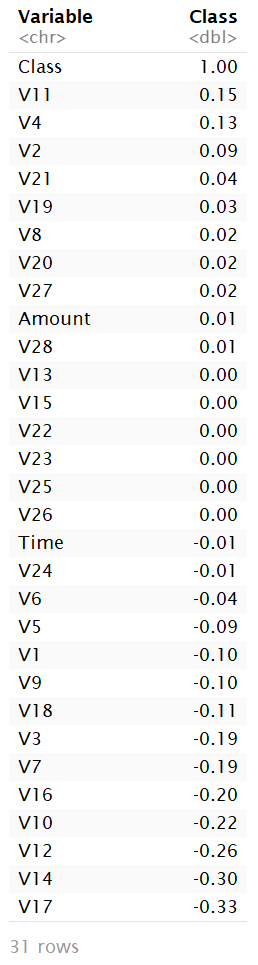

A majority of variables exhibit normal distribution and do not require the log transformation - it is likely they have been pre-normalized for this exercise

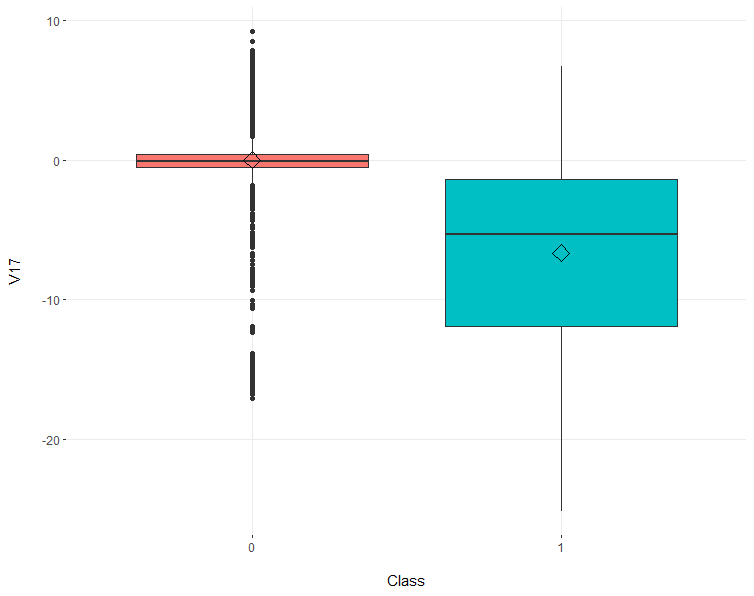

V17, V14, V12, V10, and V16 exhibit negative correlation coefficients above abs(0.2)

Summary

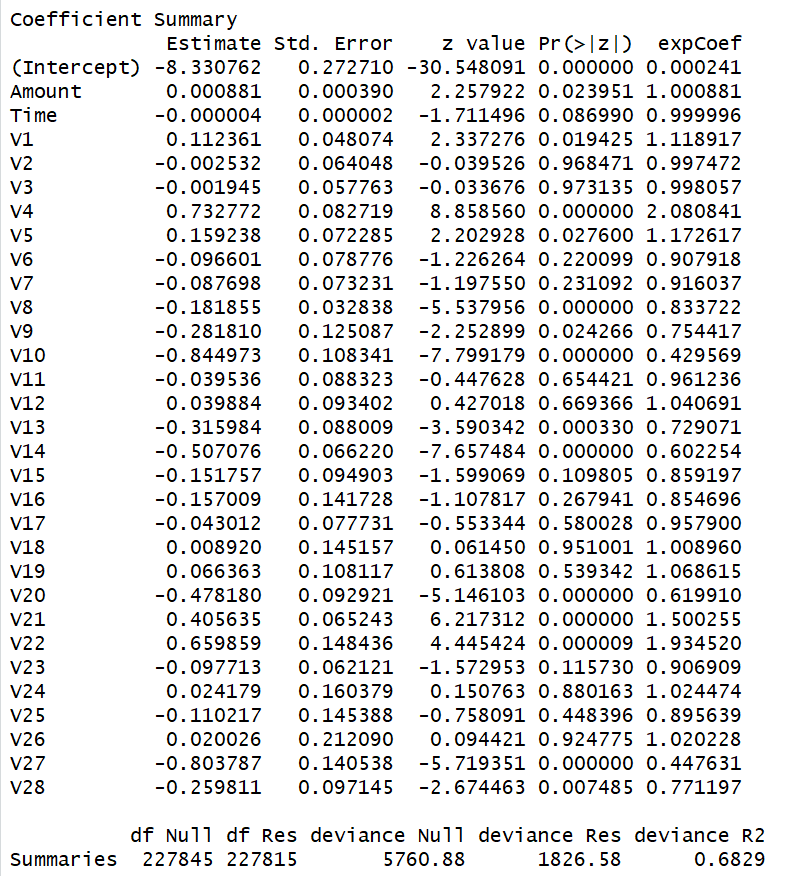

First Model: kitchen sink approach

Using all variables to run the first model shows promising results but likely overfit (too many variables). FirstModel <- glm(Class ~ Amount + Time + V1 + V2 + V3 + V4 + V5 + V6 + V7 + V8 + V9 + V10 + V11 + V12 + V13 + V14 + V15 + V16 + V17 + V18 + V19 + V20 + V21 + V22 + V23 + V24 + V25 + V26 + V27 + V28,family = binomial(logit), data = CCFTrain)

Quality

Res Deviance: 1826.58

Null Deviance: 5760.88

Deviance Pseudo R²: 68.3%

Accuracy

Threshold: 0.5

Recall: 61.89%

Precision: 88.32%

Summary

Poor performance despite the good quality metrics, there are many variables with no significance that can likely be removed.

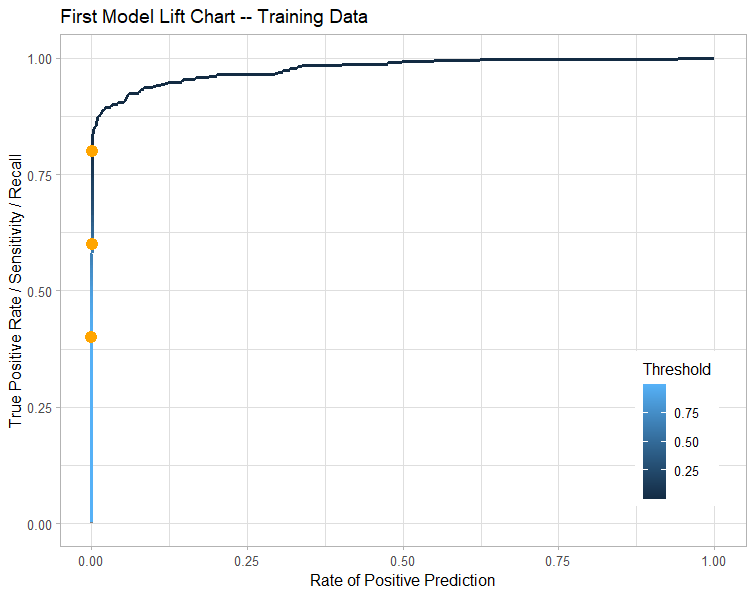

We need to evaluate 5% of the population with high probability of fraud to capture 80% of the fraud cases

Variables V4 & V22 increases the likelihood of CC Fraud by 2x

V10 & V27 decrease the likelihood of CC Fraud

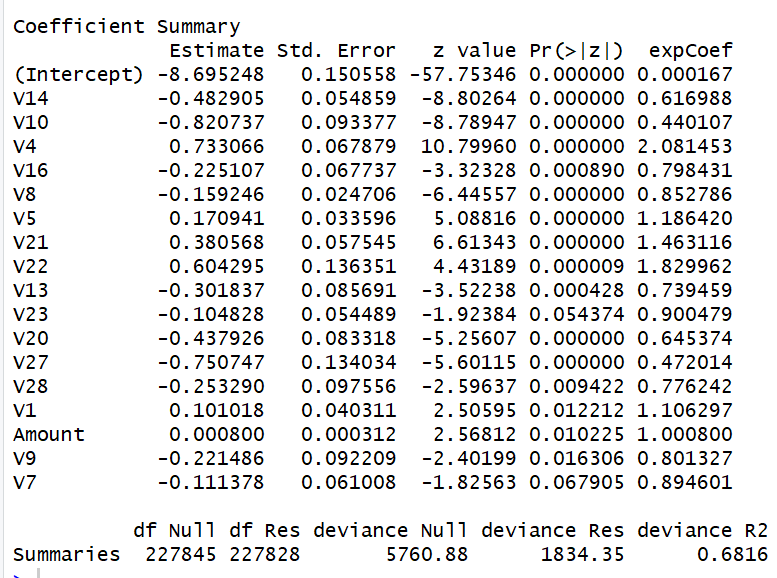

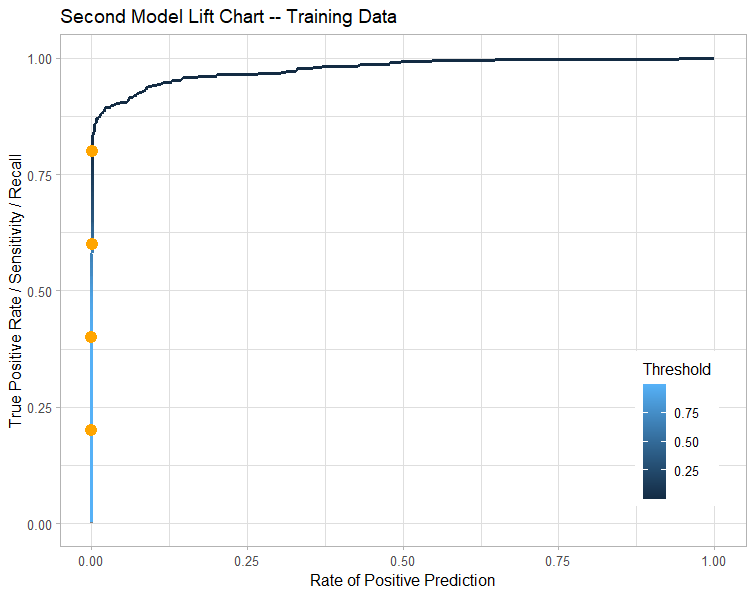

Second Model : running the stepwise function

The stepwise function returns 16 variables out of the 30 with similar results to the First Model. This function removes variables one by one (likely ones with no significance (p<0.05)) and reruns a new model each round to land at the ‘optimized' model performance.

Quality

Res Deviance: 1834.35

Null Deviance: 5760.88

Deviance Pseudo R²: 68.2%

Accuracy

Threshold: 0.5

Recall: 61.38%

Precision: 88.24%

Summary

This model is much improved by the reduction of non significant variables. But there is potential to continue removal of variables with smaller impact on detecting CC Fraud - those with coeff ~1.

We need to evaluate 5% of the population with high probability of fraud to capture 80% of the fraud cases

Variables V4 & V22 increases the likelihood of CC Fraud by 2x

V10 & V27 decrease the likelihood of CC Fraud

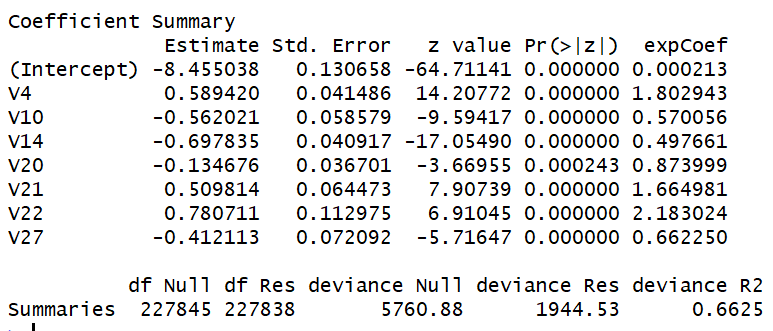

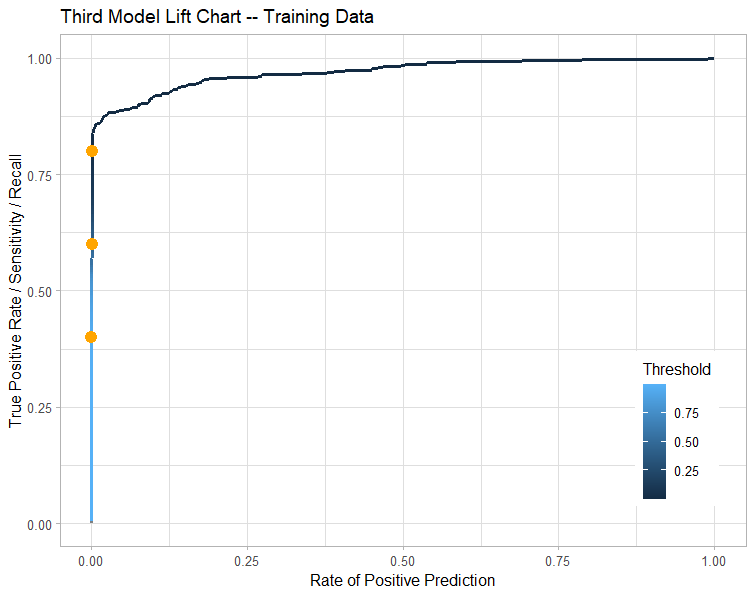

Third Model: self selection

Based on the outcome above from the stepwise function, we can run a third model, reducing the variable count to 7, roughly half of the above model and still retain decent results. I selected variables with coefficients further from 1:

ThirdModel <- glm(Class ~ V4 + V10 + V14 + V20 + V21 + V22 + V27, family = binomial(logit), data = CCFTrain)

Quality

Res Deviance: 1944.53

Null Deviance: 5760.88

Deviance Pseudo R²: 66.3%

Accuracy

Threshold: 0.5

Recall: 58.31%

Precision: 86.69%

Summary

I lost 3% of recall and ~2% of precision by cutting the variable inputs by half, so maybe not a major loss for a model that shows more clearly which variables are the most important.

We need to evaluate 4% of the population with high probability of fraud to capture 80% of the fraud cases

Variables V4 & V22 increases the likelihood of CC Fraud by 2x

V10, 14 & V27 decrease the likelihood of CC Fraud

Finding the right Threshold

In the previous models I was using a default Threshold of 0.5. The Threshold is the value above which the data point will be considered positive (or CC Fraud detected) on a scale between 0 and 1. Recall (aka True Positives of CC Fraud) measures the amount of true positives divided by true positives + false negatives (aka the total observed amount of CC Fraud). Precision measures the amount of true positives divided by trust positives + false positives. Accuracy measures the overall correct predictions of the model divided by the total data points. Calculating the F1 Score can determine the best threshold for balance between recall and precision.

Threshold = 0.6, F1 Score = 0.68

Threshold = 0.5, F1 Score = 0.70

Threshold = 0.4, F1 Score = 0.69

Based on the above, the threshold of 0.5 is actually the best suited line to draw in the sand to push the output into either 1=Fraud, or 0=No Fraud.

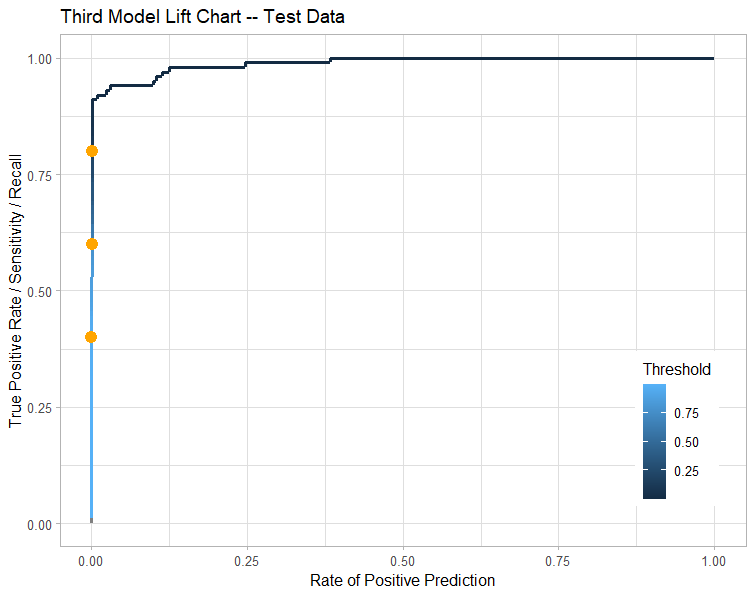

Checking the model with TEST data

Running the test data (I split the original data between 80% train, and 20% test) through the third model to see how well the model performs with a new set of data. By testing the model against the test data we can confirm that the model is consistent with different data points.

Accuracy

Threshold: 0.5

Recall: 64.36%

Precision: 82.28%

Summary

Some minor moves in recall and precision, but I believe the moves are not enough to justify that this model should be thrown away.